Supply and demand are two of the most fundamental concepts in economics. At their core, they represent how producers and consumers interact in markets. This article will provide a conceptual overview of supply, demand, and the laws that govern their relationship.

What is Supply?

Supply refers to the amount of a good or service that producers are willing and able to sell at various prices during a certain time period. The supply of a product depends on several factors:

- Production costs: Suppliers take into account the costs of materials, labor, transportation, and other expenses required to produce the good. The higher the costs, the less willing they are to produce and supply at a given price.

- Technology: Improvements in production technologies and processes can increase efficiency and decrease costs, enabling suppliers to boost supply at the same or lower prices.

- Number of sellers: The more firms there are in a market selling a particular product, the greater the overall supply.

- Taxes and regulations: Government rules that make production more difficult or costly tend to restrict supply.

- Prices: When the selling price rises, suppliers are incentivized to increase the quantity they supply.

What is Demand?

Demand refers to the amount of a good or service that consumers are willing and able to purchase at various prices during a period. Demand depends on several factors:

- Consumer preferences: The higher the desire for a product, the more of it consumers will look to purchase. Tastes and preferences vary by consumer.

- Income levels: Consumers’ purchasing power depends largely on disposable income, or how much money remains after taxes and necessities. Higher income levels drive up demand.

- Prices: Contrary to supply, demand moves inversely with price. When prices fall, consumers will demand more. When prices rise, demand falls.

- Number of buyers: The larger the target market for a product, the greater the overall demand.

- Availability of substitutes: Consumers are less dependent on one particular item if many alternatives exist in the market.

The Supply and Demand Relationship

Now that we have defined supply and demand individually, how do they interact in markets? The basic premise is:

When demand is greater than supply, prices tend to rise. When supply exceeds demand, prices tend to fall.

Suppliers want to maximize profit by selling at the highest price the market will bear. Consumers want to pay the lowest price possible for the goods they want. The supply-demand relationship seeks equilibrium – the price point where the quantities demanded and supplied are balanced.

This interaction creates the market forces that drive price discovery. If there is disequilibrium where supply exceeds demand, suppliers will compete to attract buyers by lowering prices. Excess supply causes downward pressure on prices.

Conversely, when demand outstrips supply, consumers bid against each other and drive prices up. Shortages lead to upward pressure on prices.

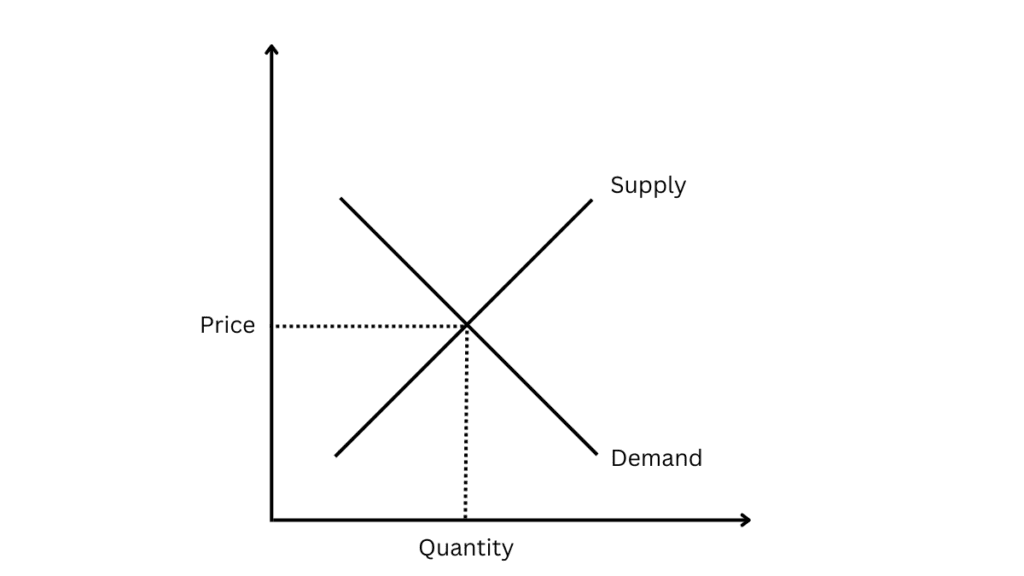

When the forces reach equilibrium, prices stabilize. The market clears – buyers wanting to purchase at the market price find willing sellers. This equilibrium is indicated by the “X” formed in the graph below, where the supply line intersects the demand line at a certain price and quantity point.

The Laws of Supply and Demand

While individual supplier and consumer behaviors are complex, the aggregate forces of supply and demand tend to follow certain economic laws. These laws describe typical responses to various events in the marketplace.

Law of Supply

The law of supply states that, all else being equal, the quantity supplied rises as prices increase and falls as prices decrease.

Suppliers are motivated by profit. When prices rise, they can earn more per unit sold, incentivizing them to boost production and bring more supply to market. As prices drop, profits decline, and they will supply less.

Law of Demand

The law of demand says that ceteris paribus (Latin for “all else being equal”), the higher the price, the lower the quantity demanded. And vice versa – lower prices increase the quantity demanded.

Consumers look to maximize utility or satisfaction. As prices increase on a good, it provides less utility per dollar spent. So consumers will look to purchase smaller quantities at higher prices.

Law of Demand and Supply Equilibrium

The equilibrium price and quantity for a product are reached when the laws of demand and supply intersect. At this equilibrium point, the amount that buyers want to purchase exactly equals the amount producers want to sell.

If the price is above equilibrium, supply will exceed demand, driving the price down. If the price is below equilibrium, demand will outstrip supply, pushing the price up.

For example, suppose the equilibrium price for coffee mugs is $10 and 100 mugs are supplied and demanded daily at this price. If the price was set at $15, suppliers may provide 150 mugs while only 75 consumers will look to buy them. The excess supply would force mug prices lower.

Law of Diminishing Marginal Utility

While the law of demand illustrates the inverse relationship between price and quantity demanded, diminishing marginal utility explains the consumer behavior behind this phenomenon.

As a person increases consumption of a product, each additional unit is less satisfying than previous units consumed. The first cup of coffee in the morning provides more utility than the third or fourth cup.

Due to this declining additional utility, consumers will only pay less for each additional unit. The price must drop incrementally to justify continued consumption. This principle underpins downward-sloping demand curves.

Factors Shifting Supply and Demand Curves

While the laws of supply and demand tend to hold true on average, there are circumstances that can cause the curves to shift position. What factors might lead to such shifts?

Factors that Increase or Decrease Demand:

- Changes in income – Higher incomes shift demand out (right on a graph), and lower incomes shift demand in (left on a graph).

- Changes in related product price – A lower price for coffee makers may increase coffee demand.

- Consumer tastes and preferences – Trends like health consciousness can increase or decrease demand.

- Number of consumers in the market – More consumers means higher demand.

- Consumer confidence – Optimism about the future boosts demand, pessimism dampens it.

Factors that Increase or Decrease Supply:

- Input costs – Higher material costs shift the supply curve in, lower costs shift it out.

- Technology – Productivity enhancing technologies allow more supply at lower prices.

- Number of producers – More sellers increases market supply.

- Taxes and regulations – More burdensome rules restrict supply.

- Producer expectations – Anticipation of higher prices in the future increases current supply.

These factors cause the supply or demand curve to shift right or left. The intersection of the new curves will establish a different equilibrium price and quantity.

Real World Examples

How do the laws of supply and demand play out in real scenarios? Here are two common examples:

Gasoline Prices – Rising crude oil prices increase the production costs for gasoline, decreasing supply. Simultaneously, increasing global demand shifts the demand curve outward. Lower supply and higher demand leads to rising fuel prices at the pump.

Stock Market Crashes – During a market crash like 2008, uncertainty causes demand for stocks to plummet rapidly. At the same time, many shareholders rush to sell off stocks, drastically increasing supply on the market. Excess supply coupled with lower demand brings about falling share prices.

The laws and principles governing supply and demand provide a framework for analyzing a variety of economic observations. While the scope here was conceptual, this overview helps explain market behaviors using some core economic concepts. Understanding foundational theories can improve practical financial and business decision-making.

Further Reading

Looking to gain a deeper understanding of supply and demand concepts? Here are some insightful book choices:

- Thinking Strategically: The Competitive Edge in Business, Politics, and Everyday Life by Avinash K. Dixit and Barry J. Nalebuff – An engaging book that relates game theory and competitive strategy to supply and demand concepts.

- Naked Economics: Undressing the Dismal Science by Charles Wheelan – A fun, accessible book that breaks down key economic principles for the everyday reader.

- Freakonomics: A Rogue Economist Explores the Hidden Side of Everything by Steven D. Levitt and Stephen J. Dubner – An entertaining read that demonstrates core economics by examining obscure real-world data.

Pairing the concepts from this article with deeper dives provided by these books can take your supply and demand knowledge to the next level. Understanding these foundational economic models provides a strong base for future learning.

This post may contain affiliate links, which means I may receive a commission if you click a link and make a purchase. However, my opinions and recommendations remain my own, uninfluenced by any potential earnings.

Before you go…

- Subscribe via email to receive future articles and updates.

- Share this post with friends and colleagues who may find it insightful.